Fifteen Personal Finance Tips For Young Adults That No One Is Talking About

This is the Off Brand Guy’s most epic post to date. We have put together a comprehensive list of the best personal finance tips for young adults. To be frank, a lot of the personal finance information floating around the internet and social media is just fluff. It is not actionable. Or it is just trying to sell you something. I have reflected on the best practices I picked up throughout my twenties. Some of these are simple and some require a bit of work and effort. Here is the thing. These are all actionable. These are personal finance tips that real people can apply to save money, build wealth, and live a better life. Let’s go!

1. Protect Your Finances

This is typically a topic people ignore people it is boring. I agree. It is more fun to focus on ways to increase your income. People prefer to read about new investments ideas or popular side hustles. I get it. But you have to stop and think about the downside. You have to consider worst case scenarios. This should be at the top of the list personal finance tips for young adults.

I recently had two family members lose hundreds of thousands of dollars which they invested with a friend. To everyone’s surprise the guy had pretty much been running a Ponzi Scheme. In hindsight, he had clearly been losing money for over a decade. Rather that admit defeat. He started taking more money to pay back current investors. This wasn’t some random guy either. He was a close family friend. He was known in the community as being smart and financially sophisticated. It was all a lie. A financial lose like this can change everything.

This isn’t the only type of thing to be on the look out for. How about theft? A year or so back the shed in my front yard got broken into. Someone cut the lock. I ended up finding it on the ground in the dirt. The good news is we didn’t really have any valuables in the shed. The main loss was a pressure washer worth a couple hundred bucks. This incident was a surprise because we live in a nice area with minimal crime. I always thought a security system would be overkill. I was wrong.

My point is that a lot of different things can happen to you and your family throughout life. Unpredictable things, that can have a devastating financial impact. In addition, to thinking about being frugal and saving money you have to take some time to reflect on how to protect the wealth you do have. Let’s take a look at a few of the things I have implemented in my life.

Understand FDIC Insurance And Coverage Limits

The first thing I started reflecting on is where I keep my money. Could I be victim of fraud? Following the bank runs during the Great Depression the government added FDIC protection for consumers. If a bank was to fail each depositor is insured up to $250,000 per bank for funds in a savings account. Here is the thing. I don’t really keep that much money in savings. I like to invest my money. Especially in an era of almost 10% inflation.

I do feel secure having my funds in a major brokerage. While my individual investments are not FDIC protected. A lot of things would have to go wrong for my money to be in jeopardy. But here is the thing. I wonder if many investors at FTX felt secure because the size of the firm. Another reason to do your due diligence and be careful out there.

How Can I Protect My Personal Finances?

Home Security System

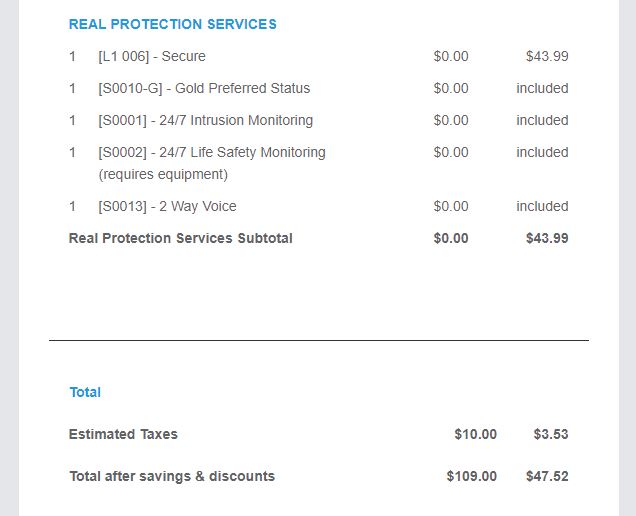

After the break in, I decided it was time to get a security system. I hated the idea of some criminal walking about my property trying to find some low hanging fruit for a quick snatch. I looked at two options. The first was an ADT home alarm system. The previous owners of our house had an ADT system, so we had the hardware already setup. To be frank, I was not impressed with the experience. I called customer service and asked for pricing. They told me I had to talk with the local sales rep. They said it was impossible to get pricing without doing so. I requested a virtual meeting (because this was during the pandemic). The sales rep called me thirty minutes before our appointment time and said he was on his way over. I reminded him again that it needed to be a virtual appointment. He was slightly irritated but ended up accommodating. All in all, the thirty minute meeting was a long overview trying to convince me to get a new system. And even if I wanted to activate the current system, it would have to be officially inspected. Of course, at a significant fee of a couple hundred bucks. The monthly plan was around $48 after taxes. To me this seemed overpriced. I decided to explore alternative options.

Oh, and the sales rep kept calling and calling and calling. Then I got an email from a manger, and then from a higher level manager. This old school sales approach is outdated. No one wants to go through this just to get a home security system.

Related: SimpliSafe Coupon Code – Affordable Home Security

I ended up connecting with SimpliSafe. I got all the hardware for a couple hundred bucks. This even included a security camera that I mounted outside. The monthly plan is around $15 a month. To me the price was right. There are two options for getting the hardware setup. You can do it yourself or pay about $100 to have a 3rd party contractor come out and assist with the setup. We wanted it done right so we went with this option. They sent out this nice, sort of goofy, older gentleman that came out and spent a couple hours implementing the sensors. After watching him, I am sure we could of done it ourselves.

In general, a security system brings piece of mind. This is especially important to me when I am traveling. I have worked hard to buy the things I own. I can’t stand the idea of someone trying to get into my place to take this stuff from me. Home alarm systems aren’t bulletproof. Once the police are dispatched it would take them a few minutes to arrive. But any burglar would quickly realize they didn’t have much time.

Paper Shredder

Next up, the importance of a simple paper shredder. Can this really improve your personal finance situation? Let’s take a look. I go to FedEx for work a lot. It always cracks me up when I see some elderly person getting their junk mail shredded. Rather than pay to do this at the store, you can spend $30 or so and get a paper shredder on Amazon. Honestly, sometimes I am too lazy to shred all my stuff. But I do it for the important documents. Identify theft is a big deal. I personally have never been a victim. But I do hear horror stories.

My closest experience with attempted identify theft was while traveling in Paris a couple years back. We were walking outside the Louvre. I made the stupid mistake of having an American college football shirt on. This made me a clear American tourist target for the thieves. Two teenagers came up to us with a clip board as if they were collecting signatures for a petition. Before we could tell them were not interested they bumped into my wife and grabbed her phone. And then ran off.

We immediately took action to disable the phone. The problem is that the thieves were relatively sophisticated. They quickly tried to get into her Facebook account. We spent the next year or so looking over our shoulder for potential signs of identity theft.

The most important thing is to be careful. You don’t need someone outside your house trying to collect personal information. It is challenging to be perfectly secure. But shredding mail and personal documents is an easy first step to protect yourself.

Password Manager

I had been avoiding this for years. I am so glad I finally got it implemented. My main excuse was that I have many devices including a work phone and computer. I knew I wouldn’t be able to put a password manager on my work devices. I travel a lot and figured this would defeat the whole purpose. Then I had a family member purchase a subscription to Keeper. Now, with free access to premium password manager service I had no excuse.

The setup process was painful. But so worth it! Now, all I have to do is remember one password.

I started by just adding my most important accounts. It takes time to add a new password. So I didn’t want to do this for every random account. But for banks, credit cards, and frequently accessed subscriptions. Absolutely.

These password manager services accomplish a couple things. First off, they automatically make long random password that you would never be able to memorize manually. Secondly, they have services that scan the dark web to make sure your current passwords are not floating around in shadowy places.

Things have changed a lot in the last twenty years. Going back to 2000, most people had very limited personal information floating around online. That has all changed. Now, passwords and online security are a big part of protecting your financial life. I see older folks who have robust home security system, big fences, and other physical protection. But then use the same “something123” password for all their accounts. This is a huge mistake.

Life Insurance

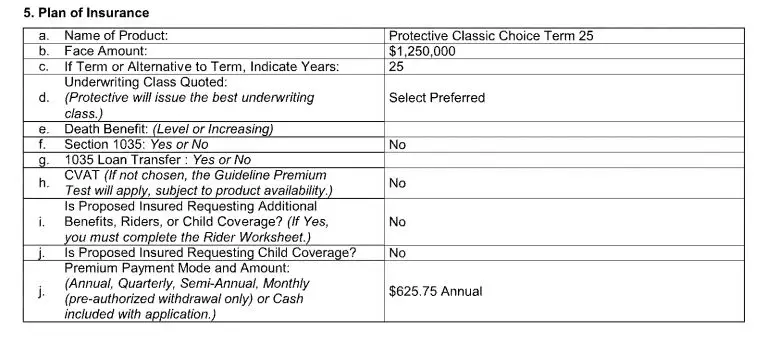

I decided to get life insurance once I hit thirty. It was earlier than I probably needed it. I didn’t have kids yet and I had enough savings for my wife if I passed away unexpectedly. My work offered a basic plan for free. They take your highest salary from the last five years and multiply it by two. The more I started thinking about it this not enough. I had a family friend get cancer in his early thirties. Once something like this happens you are uninsurable. This motivated me to move forward and get a plan in place while I was still healthy. Yes, I could of probably waited five more years. But I wanted piece of mind.

I spend a lot of time reviewing the policy options. Too much time. I hated the idea of shelling out a bunch of additional money to an insurance company each year. Also, for something that seemed completely optional. I reviewed all types of policies and decided on term life insurance. The “whole life policies” seem like a scam to me. The insurance sales person will try to talk you in to thinking of it like an investment. If I am going to invest money, I can just do it my self. Plus, the policy amounts were kind of worthless. Why go through all the trouble of setting up a policy just to get my family a $100,000 if I die? The reality is that these plans are riddled with commissions and fees. They are lucrative so the insurance companies push them hard. Focus on “term life” polices.

I settled on a twenty five years policy at around $50 a month. This was a 1.25M policy. I probably could of got away with a twenty year policy. I hope to be financially secure and independent by fifty. But I got a twenty five year policy just in case I have children in college. You definitely pay a premium for coverage during the 50-60 age range. Obviously, this is when you are more likely to have a health issue. Coverage in your thirties and forties is much cheaper.

Life insurance is serious stuff. You have to go get bloodwork done and go through an interview. Insurance companies don’t want to protect people that are statistically likely to pass. They want to make sure you don’t smoke and that you don’t engage in high risk activities like mountain climbing.

The nice thing is that once this is done you sort of forget about it. As times passes the monthly premium become more insignificant with inflation. The same for the principal payout. But that is another matter. The piece of mind is worth the time and money.

Long Term Care Insurance

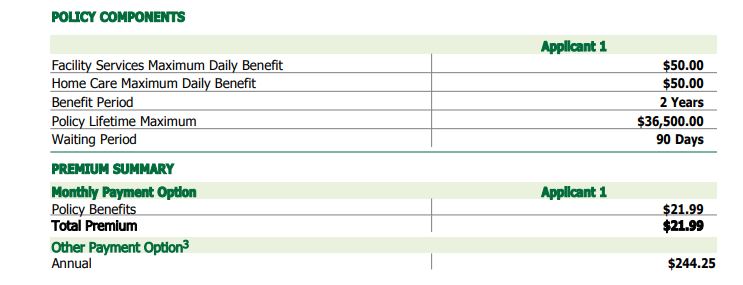

To recap, LTC insurance provides coverage for the costs associated with the activities of daily living such as eating, bathing, dressing etc. if you suffer from a chronic illness or injury. Personally, I think Long Term Care (LTC) insurance is sort of a scam. Like it use to be valuable back in the early 2000’s. The companies offering these policies underestimated just how expensive it would be to cover the plans. This means customers were underpaying for the premiums. Now, this has all changed. Now, insurance companies realize just how expensive it can be to cover someone especially with how long people live these days.

Many policies only cover the costs of your long term care for 2-5 years. To me this doesn’t make sense. If you suffer a serious injury, you may need care every day for the rest of your life. To go out of your way to get an insurance policy to protect yourself that only kicks in for a couple years seems like a waste of time.

I recently got a LTC policy due to legislation passed in the state of Washington. The state is implementing a payroll tax of 0.58% unless employees already have implemented a private LTC policy. The state sponsored plans offer Washington residents up to $36,500 to cover the costs of long term services and support.

My private plan through New York Life is only about $250 a year. It provides the same level of coverage as the state plan and based on my income it will cost less. The government can barely handle it’s currently responsibilities. It does not need to be meddling in LTC coverage.

Disability Insurance

Disability insurance is another topic that may not seem super exciting. But it is important to think about. Unpredictable things happen in life and you have to be prepared. I personally don’t have this type of coverage. I did explore coverage through my employer and through the private marketplace. The plans were just too expensive. If I remember correctly at the minimum the premiums were around $2000 a year.

On the other hand, my wife does have coverage. Her employer offers a competitive plan that would cover up to 60% of pay. The key thing is that the premiums are reasonable. She has some health issues that make this type of coverage more important. Also, it could be applicable if we have children. The important thing is to at least explore the options and then decide what makes sense based on your family circumstances.

How Much Homeowners Insurance Do I Need?

If there was more financial education in the public K-12 system then maybe we wouldn’t need to cover this. Unfortunately, this is not the case. When we first purchased our house, I was overwhelmed with figuring out homeowners insurance. I didn’t have as much time as I wanted to research the details of the plans because we had to move fast. Over time, I have developed a better understanding. Here is what I have learned.

First off, good home owners insurance matters. Your home will be the biggest purchase you ever make. You need to protect it. At the same time, the insurance companies take advantage of customers. They increase the coverage amounts each and every year until the coverage balloons beyond what is really necessary.

We bought our house from my wives’ parents. We reviewed their policy when we went through this process. The annual premium of their policy was around $1800. We ended up paying around $1100. They hadn’t shopped around over the years and the insurance company slowly increased their coverage every year until it really didn’t make sense.

The premium of a homeowners insurance policy is based on the following coverage:

- Dwelling

- Personal property

- Personal liability

- Loss of use

- Other structures

- Medical payments

The cost will mostly be dedicated by the coverage amount for the dwelling and your personal property. This is the big ticket part of the coverage. Speak with a few different insurance companies. Go through the details of your house and see what level of coverage they recommend. Then you can look at each of these coverage amounts and make sure you are comparing apples to apples.

You need to understand the different components of the coverage. If you take your policy from one company and try to shop it with another company for a better price, sometimes they will just lower a specific coverage amount. For example, they may reduce the liability coverage from 200k to 100k. Then they will tell you that they can provide a lower premium. In reality, all they are doing is lowering the coverage.

Now, let’s talk about the personal liability part of the coverage. This is the one part of the coverage I would increase well beyond the minimum. Many plans start at $100,000 or $300,000. If you have any type of assets, I would increase it well beyond this. It doesn’t cost that much. Personal liability insurance typically costs around $8-$10 a year for every $100,000 of coverage. This part of the coverage protects you “for claims of bodily injury and property damage sustained by others”.

Related: How To Get The Lowest Home Loan Interest Rate?

Do You Save Money When You Bundle Insurance?

Many insurance companies advertise about bundling coverage. I will say this can be convenient. But frankly, it rarely provides significant cost savings. Companies move the costs around and try to portray that you are getting a deal. They play to their strengths. For example, I was originally with Amica for homeowners and Geico for car insurance. The homeowners coverage was really competitive the first year. Then is went up substantially. They told me they could lower it if I bundled my auto insurance. At first, this seemed promising. Then I saw that their auto rates were twice as much as Geico. All they were doing was moving costs around.

Do You Get A Discount For Having An Alarm System?

This can be misleading. As you know, I am a big believer in security systems based on their own merits. Insurance companies will highlight the discounts you get for having a security system. In reality, this is marketing to make you feel like you are getting a deal.

How To Build An “In Case Of Death” Binder?

I am not at the point in life where I have taken the time to put together a will. I will probably get around to this in the next five years or so. But what happens if I was in an accident? I have worked hard for the assets I have. I don’t want things to be mess if I unexpectedly die. I want to make sure my assets would properly get to my wife, my brothers, etc. This is not what comes to mind for most people when they think of personal finance tips for young adults. But it is important.

I spent an afternoon thinking about this. I put together a list of instructions and provided this to my wife and brother. It instructs them on where my important documents are located, what accounts I have, how to access the accounts, what insurance coverage I have in place, where these documents are located, and so forth. Other wise, how would anyone know? A lot of this information was only in my head. It was a strange document to put together, but I was glad I got started. I figure I can slowly add to this as my life progresses.

How To Keep Important Documents Safe At Home

Being a victim of a home break in or financial fraud makes you consider the bigger picture. An important part of financial security is being organized and protecting your important documents. I recommend SentrySafe. A home safe is not something to cheap out on. You want to find a quality brand and something that is water and fireproof. Most people go out of their way to protect things like cars and collectibles but forget about the documents that matter most.

What Documents Should Be Kept In A Safe?

- “In case of death binder”

- Passport

- Birth certificate

- Marriage certificate

- Financial documents

- Insurance documents

- Computer backup

- Social security card

- Will

- House documents

- Car title

2. Learn To Be A Smart Shopper

I am not going to talk about budgeting and all of that. That type of financial advice is overdone. Yes, budgeting is important and part of personal finance 101. But I want to go a step further. Do you reflect back on previous purchases? Do you think long term? Most people go about their day and just buy stuff when they feel like. Their vacuum cleaner breaks so they go to the store and grab the one that is eye level on the shelf. I recommend putting in a little effort and being strategic.

Related: Products You Should Buy Generic

Over the last few years, I have purchased new kitchenware, new kitchen knives, a daybed for the living room, a dining room table, and a few new lamps. I plan on having this stuff for awhile. It was a slow gradual process. I read reviews over a period of time. I thought about the different features that were important to me. I thought about what the future looked like. Would me tastes and preference change over time? Would the items I was considering purchasing hold up over time?

Most people think it is frivolous to be so methodical when buying stuff. Honestly, the opposite is actually true. Social media has tricked people into thinking their lives are extremely important. People think it is cool to just consume aimlessly. No point in thinking about things too much. This is childish. This is not the route towards accumulating wealth.

The second part of being a smart shopper is documenting your purchases and savings receipts. You should be able to locate the records for medium and large purchases. It doesn’t take that much work. Keep a folder for product manuals, and a folder for receipts. I keep a hardcopy folder and have folders within Gmail for digital files. Whatever works for you. When you buy quality products (like Wusthof or Shun kitchen knives) from reputable brands you will be surprised at how accommodating they are in making sure you are happy with the purchase. Never assume anything. If a product is not working right always, check with the manufacturer about a repair or replacement.

Related: Walmart Return Policy – A Walmart Shopping Secret

3. Learn Basic Home Maintenance And Repairs

I have a friend who is the handiest guy I know. He can pretty much fix anything. I asked for him his secret? Whenever he has to make a service call for a home repair he follows around the repairman. This may sound silly. But it is a genius idea. Many home repairs are not really that sophisticated. It is more about developing the skillset and understanding what tools are needed.

You would be surprised at how helpful people like HVAC tech, plumbers, and appliance installers, will be to answer you questions. I always have a list of questions and make sure to take notes. Service calls are expensive. I figure I might as well get the most value out of the visit. It is the smart thing to do.

Related: How To Save Money On A Furnace Filter Replacement?

Also, it is important to be strategic with service calls. I know some people who don’t really give this much consideration. Not every issue needs an electrician or a plumber. Sometimes a more basic level of service will get the job done. Plus, always make at least three calls to get pricing. In my area I always see commercials for Beacon Plumbing. They advertise like crazy. They get players from the Seahawks and have excellent brand awareness. This means they are the company that the average Joe remembers when a plumbing issue comes up. This means you will overpay on your bill to support this big advertising budget. Do your research on home maintenance and repairs.

4. Track Reward Miles & Credit Card Points Over Time

Now, to a more fun personal money management tip. I have went through periods where I have been really into hotel, airline, and rental cards points. I aimed to squeeze every possible dollar out of these programs (like when I stayed at the Hilton Waikoloa Village for free). This worked out pretty well. I have taken a big international trip every July at a fraction of the retail cost. Here is the thing. Optimizing travel points is complicated and time consuming.

The hotel and airline companies want it to be this way. The idea is to change the program all the time to keep customers engaged. That is way you get emails asking you to opt in to a specific promo or enroll in a special offer. Engagement is good for building customer loyalty and retention.

Related: Walmart e Receipt: Save Money By Storing Receipts

How To Make The Most Of Your Hotel Reward Points?

So first off, you have to play the game to maximize earning points during your travels. The big one is for hotels like Hilton and Marriot. A good chuck of rewards points come from the promotions. This is things like “on stays through June of this year earn 2000 bonus points per stay by opting into this promotion”. You have to track and opt in to these promotions for the points to really rack up.

But here is the key message I want to get across. Track point redemptions over time. Personally, I have a Gmail folder where I store any trip I take with points. This only takes a second. But it makes my life so much easier in the future. As program change, and redemption offers to certain destination fluctuate, I have a benchmark to look at. This is the best way to become an expert at any given loyalty program. Yes, you can always search around online. But with how fast things change this method does not work out very well.

5. How To Put Your Groceries On Auto-Pilot

You will find that a few of the tips on this list revolve around grocery shopping. There is good reason for this. According to Earnest, “financial advisors and gurus recommend spending no more than 10%-15% of take-home pay on food, a figure that includes restaurant dining and takeout”. That is big chunk of your spending that is never going away.

Related: Eight Off Brand Products Better Than The Name Brand

How To Manage Money In Your 20’s?

An important skill to develop as a smart shopper is to put in the research up front and then effortlessly make the same purchase again and again. I spent my early twenties figuring out which grocery stores products I preferred and which were the best value. Also, I identified the things I liked spending a little more on (coffee and craft beer!) Now, I can just make repeat purchases of these items whenever needed.

I like shopping at Walmart, Costco, Trader Joe’s, and Safeway (sometimes the Dollar Tree too). I shop at Safeway because it convenient. If you pay attention to what is on sale and engage with the Safeway Just For You coupon program you can find good deals. During the Covid pandemic we got in the habit of submitting online orders for pickup. Amazingly, this is free! On Saturday, we make our list for the week and then just swing by the store on Sunday to pick everything up.

The nice thing about online orders is the system remembers what items you like to order. They show up at the top of list which makes it easy to compare prices and make repeat purchases. Don’t be the frugal personal that reevaluates every purchase every time you go to the store.

6. Don’t Try To Time The Market

A young person’s guide to investing could be summed up with the statement “investing should not be complicated”. A consistent and simply strategy is the best approach. The mainstream media covers topic like derivatives, synthetic shares, meme stocks, short sells, etc. This is not stuff the average person should be getting involved with. Also, in my experience more complexity leaves room for fraud and manipulation. Identify low cost, broad market index funds and set a reminder to dollar cost average. You will never have regrets with this approach. The market will go up and down over time and you will not have to worry if you made the right choice.

For the most part, I have done a good job with investing. Though, I did find myself getting caught up in the post Covid pandemic stock market boom. I decided to get more into technology stocks. Not necessarily because of Covid but because I was starting to think more long term. I am in my thirties and I was thinking about what the next twenty years would look like. I had built a portfolio of diversified index funds and I thought it was my chance to get in on the next Amazon, Tesla, or Netflix.

So I decided to do some stock picking. My timing was terrible. Not the individual picks. But just the timing. This was right at the beginning of 2022. I broke away from my usual dollar cost averaging strategy and went hard into some individual stocks. I regretted it immensely. It is so hard to see freshly invested money down 30% or 40%.

Even though it was tough I stayed patient and committed to my strategy through the rocky 2022 market. I continued to invest in the companies I had selected and it looks like it will work out fine. But it wouldn’t have been so painful in the short term if I hadn’t tried to time the market.

7. News Source That Are Worth Getting A Paid Subscription

Many personal finance bloggers will tell you to cancel subscriptions to save money. I get what they are saying. Many people are signed up for services they have long ago forgotten about. But here is the thing. You should be paying for a quality news service.

Media has changed. The news you can get for free is horrible. You are the product. The headlines are clickbait and only serve to get your eyes on advertisements. Spend a few bucks and subscribe to news publications like The Economist and Barrons. This is a small investment that will pay dividends over time. Time is valuable. The coverage from these organizations will not waste it. Otherwise, you will come to think the world revolves around Kim Kardashian, Jake Paul, or whatever celebrity is currently making headlines.

Also, look at advice coming from real people going through similar situations. Reddit has some amazing personal finance advice. One of my favorites is the FatFIRE subreddit.

8. Find Satisfaction In The Simple Joys Of Life

A list of personal finance tips for young adults would not be complete with taking about “gratitude” and “enough”. It is hard to break away from our consumerist culture in the US. But it can be done. This doesn’t mean you can’t enjoy buying stuff. You just need to slow down a little bit and make sure it is truly adding value to your life. The key is the “why” behind a potential purchase. Are you being thoughtful? Is this something you have been thinking about for a long time? Will you still care about this item in a year from now? How about five years?

Many people buy stuff to impress people or solve a problem that can’t actually be solved by buying something. Don’t get caught up in social media. Spend time reflecting on your recent purchase history. Are you making purchases that align with your values and the things you truly care about? Or are you being sucked into glossy marketing?

You will hear all kinds of stuff about journaling and gratitude and this type of stuff. This is not some new age mumbo jumbo. This stuff is important. Personally, it has helped me a lot. What are some of the little things in life that bring you immense joy? Is it a cup of coffee in the morning? Is it a trip to the baseball card store? Is it being out in nature?

At the end of the day you are the only one that will be able to develop a frame of reference on what brings you happiness. Don’t make the mistake of connecting this with buying stuff. It is good to connect joy with an experience or activity. But break away from the transactional nature of buying stuff to feel happy.

Making purchases is not an accomplishment. I have a good friend that struggles with this. He tells me about a new purchase as if it is equivalent to having a baby, getting a new job, or having some type of creative breakthrough. Seriously, he is after a “congratulations” type of response. This is not good because it is not sustainable.

Related: 19 of Life’s Simple Joys

9. Figure Out What Your Health Insurance Plan Covers

Health insurance is unreasonably complicated in the US. And it seems to get more complex every year. It reminds me of my compensation plan at work. They start each year giving a pitch about how they have made big improvements to reduce the complexity. And every time the changes actually make it more confusing. That is the health insurance world too.

First off, you need to accept that health insurance isn’t something you can quickly select when you start a job. You have to take some time to deeply research the options. It is crucial that you choose the plan that is best aligned with your personal situation. For the most part, this can be summarized with two scenarios.

Either you are young, without health issues, and rarely go to the doctor. Or you have an ongoing health condition in which you take medications and regularly go to the doctor. In the first scenario is makes sense to select the catastrophe option with low monthly premiums and then fund an HSA to get a tax break on any health related expenses. Remember you can only fund an HSA if you have a high deductible plan. In the second scenario, it may be worth paying the higher premiums for the more comprehensive lower deductible option. Out of all of our personal finance tips for young adults this one may require the most work.

:max_bytes(150000):strip_icc()/how-does-health-insurance-work-f7aa9125e51f4f6698b38789ff3929c3.png)

10. Get Good At Cooking

Cooking can either be a chore or one of those things you find joy in. It is all about how it is framed. I use to treat is like a task. Something to get through so I could shovel food down. I don’t recommend this. Now, I approach things differently. I put on some music. I light a candle and pour myself a drink. I soak up the entire experience. My wife and put extra effort into planning meals we really lookforward to. Rather than having the same thing again and again.

Related: Le Creuset NonStick CookWare Is Worth The High Price!

So why is this a personal finance tip? Eating out is expensive. If you put effort into cooking good meals you will find yourself not being tempted to go grab take out every night. Plus, it is healthier. I have started to treat cooking like going to the gym. It is an activity I can focus on after work to help me unwind. This only works if you plan good meals. Otherwise, you will mindlessly grab something out of the refrigerator and be disappointed.

11. Costco, Walmart +, etc.

The Off Brand Guy is all about optimizing those little purchases (like Bagail mesh laundry bags) that you will make time and time again. In terms of personal money management tips, grocery shopping is a big one. You will be buying groceries every week for the rest of your life. I always hesitated to spend money on memberships. I never thought I would get my moneys worth. I hated the idea of paying for the privilege to shop. This was a mistake.

Is A Costco Subscription Worth It For Young Adults?

In last few years, I have joined Costco and signed up for Walmart +. The basic Costco membership is $60. To be fair, I don’t get the same value out of this as a big family. I can’t buy the the twelve pack of muffins or the jumbo pack of milk. But there are a few things I like grabbing every month. I love Costco because I don’t have to worry about the quality. I know I am getting a pretty reputable brand. I can’t say this is always true at places like Walmart. I pick up chips, coffee, sparking water, alcohol, meat, and a few other things. Shopping at Costco is a pleasant experience and well worth the $60.

Related: Safeway Just For You App Review

Walmart + has been a gamechanger. The annual cost is $98 a year. You can get items delivered at any time. And there are no shipping fees. Amazon is good for things like electronics, coffee grinders, etc. But there are many gaps. Seriously, Walmart has everything. In the past, I would have a list of a few things I needed to get. I would find a few of them on Amazon and then realize I would need to stop by the store for the remaining items. Walmart+ has changed all of that. I can get soup, chips, and other grocery items delivered right to my door.

12. Credit Card Churning Works

Credit card churning is real. It works. You can get some points and money out of it. But only for a period of time. I spent my twenties trying to get the most out of these programs. And actually with some pretty good results.

After a while the results will diminish. You will receive all of the sign up offers from the best cards. The remaining cards available on the market will have less attractive bonus offers.

The Pros And Cons Of Credit Card Churning

Credit card churning is not hard, but it can be time consuming. You have to keep track of when to cancel, when to redeem the rewards, what purchases to put on which card, etc. If you are not on top of it then you can get stuck paying for the annual fees. This defeats the whole purpose.

Plus, the credit card companies have gotten better at preventing churning. They make it more difficult to cancel a card. They put policies in place where you can cancel they card but may not receive all of the reward points.

And then sometimes redeeming the points can be a pain. Such as having to use the points through the portal of a specific credit card company. The flights or hotels may be more expensive. Plus, it is another factor to complicate the travel planning process.

13. Ignore Social Media

This one gets missed in most of the money management tips for beginners advice. Social media can be a destructive force for your finances. This is coming from someone who has grown to really appreciate new platforms like TikTok. You have to remember that this stuff is not real life. You see influencers buying a million dollar first generation Pokémon card or highlighting their aesthetically perfect kitchen.

Here is what I find strange. Most people are able to discount that reality TV is not real. But because social media is “average people” this is quickly forgotten. The key is regularly reminding yourself that social media content is a hyperreality that exists only for entertainment purposes. Do not judge your own life based on what you see.

Social Media Can Impact Your Financial Health

Everyone talks about the impact of social media on the mental health of the youth. But people forget how much this connects to purchasing behavior. Social media makes people feel insecure. What is the classic marketing pitch of most products? If you buy this you will be cool and feel better about yourself. Plus the ads are so hyper targeted these days. It makes them much more effective.

Back in the day, you could sort of just tune out TV commercials. Now, you see advertisements for products you just searched or read about the day before. This is a lot harder to tune out.

The social media companies are working on developing more features (TikTok Shop) for content creators to sell products directly on their planforms. This is big internationally and is expected to take over in the US over the next five years. Social media influencers will leverage their following and influence to sell stuff. There is no doubt about it. Live shopping and gaming are a big growth area for any social media platform. Beware!

14. Driving A New Car Will Keep You Poor

We move on to item number fourteen on our list of personal finance tips for young adults. Don’t get caught up in the car game. Personally, I don’t get why people are obsessed with cars. Trust me, no one is impressed. I was recently at the gym. In the sauna I was watching this guy endlessly browse the cars available on Carvana. I got the impression this is something he did a lot.

Cars are a functional necessity in many cases. You should buy a quality brand (like Toyota or Honda), take care of it, and then forget about it for the next 10-15 years. I see people swapping cars every year trying to justify that they are making money on the transactions. Or people that get caught up in the financing trap. This is the worst.

I once met a lady who had a Jeep that was a couple years old. She was bragging that the dealership said she was due to for an upgrade soon. She said this as if it was some sort of accomplishment. Without any further explanation, I knew exactly what was going on. She was financing the car. And the dealership probably said something along the lines of “we can get you something new and keep the payment about the same”. All this does is keep kicking the can down the road.

15. Keep A “Things To Buy” List

I read a lot of financial tips for millennials material and this point in rarely made. As you get older you get better at anticipating that time passes quickly. You get better at delaying gratification and thinking long term. Hopefully at least! One thing I have started to do is keep a list of purchases I am interested in making. Then during big sales like Black Friday, I check to see if any of the items I need are on sale. I do this for necessities like kitchen appliances that need to be replaced or updated. And for fun purchases like a new digital amp simulator for playing guitar.

Related: Don’t Overpay! Here Are The Best Cheap Guitar Pedals

Most people get caught up in sales and buy worthless items just for the sake it. If you look closely you will see that quality products don’t typically get massively marked down during sales. It is the junk stuff like an air fryer or hot dog cooking appliance. You can still enjoy annual sales while being strategic.

I am not only talking about physical items. I am a big reader and I like to evaluate sales on digital items and subscriptions. In terms of subscriptions, the cost of an incremental sale is almost zero for the company. This means these services offer some of the best deals during big sales. Lately, I have purchased credits for the local float tank and I have signed up with a subscription to Barron’s.